The increase in online payments has created a new security risk for consumers. It has put their payment-related data at risk. According to Stripe, 9,000 data breaches occur every day.

In 2006, card payment companies such as Visa, Mastercard, AmEx, Discover, and JCB came together to set up the PCI Council, which was entrusted with establishing standards to protect cardholder data.

In this blog, we’ll dive deeper to understand PCI DSS compliance, why it matters, the risks of PCI DSS non-compliance, PCI DSS levels, and the 12 requirements.

Let’s get started!

Understanding PCI DSS Compliance

In layman’s terms, PCI DSS (Payment Card Industry Data Security Standard) is the rulebook that explains how businesses should protect card payments. Whether you’re a SaaS company storing encrypted card data or a payment gateway transmitting transactions, PCI DSS is what keeps that data safe.

These security standards have been developed and maintained by the PCI Security Standards Council to protect payment data throughout the entire payment lifecycle.

If your product touches payment card data—even indirectly—you’re within the scope of PCI DSS compliance. That includes B2B service providers, cloud hosts, payment APIs, and backend processors. It’s not optional—processors and partners expect it.

Beyond avoiding fines or breaches, being PCI compliant shows your customers that you take data security seriously.

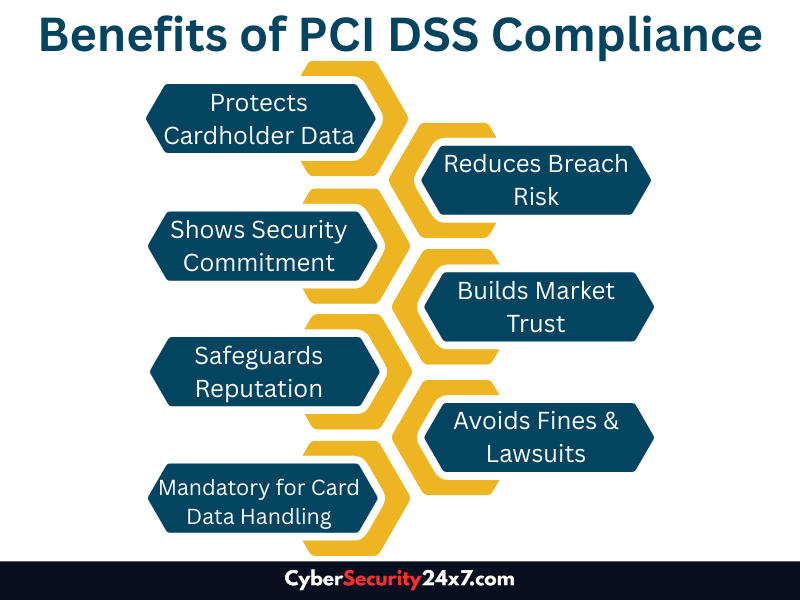

Benefits of PCI DSS Compliance

Here’s what makes PCI compliance matter, especially if you’re handling cardholder data in any serious way:

Protects cardholder data PCI DSS provides a clear set of rules for businesses to secure credit card information across systems, preventing theft, leaks, or exposure at every touchpoint.

Reduces your breach risk Enforcing strong access controls, regular audits, and encryption standards lowers the chance of a breach—and limits the damage if one ever happens.

Shows customers you take security seriously People notice when a company invests in protecting their data. Compliance tells customers you’re not guessing—you have real controls in place.

Builds trust in crowded markets When your competitors also handle payment data, being PCI-compliant sets you apart. Buyers prefer vendors who treat data security as non-negotiable.

Protects your reputation A single data breach can undo years of hard-earned trust. PCI compliance helps prevent the kind of incident that puts your name in the headlines.

Helps you avoid fines and lawsuits Payment networks can impose steep fines for non-compliance. Add legal costs, customer claims, and chargebacks—and the financial hit gets serious, fast.

Mandatory if you handle card data If your system touches cardholder data—even as a service provider—you must comply, whether or not you store the data.

Risks of PCI DSS Non-Compliance: A Real World Example

PCI DSS compliance isn’t just theoretical. Ignoring it can have real consequences. One of the most visible examples was the British Airways breach in 2018. Attackers infiltrated the airline’s systems and injected malicious code into its website and mobile app.

In just over two weeks, they stole names, payment card numbers, CVVs, addresses, and travel details from around 380,000 customers.

What caused it

British Airways had failed to secure critical parts of its site, lacked robust change monitoring, and didn’t catch the unauthorized script injection in time. These lapses violated several PCI requirements around secure development, access control, and file integrity monitoring.

Business impact

The UK’s Information Commissioner’s Office (ICO) announced a final penalty of £20 million. The company’s security posture became public knowledge overnight, and it lost the trust of many customers and partners.

The key takeaway is this wasn’t just a technical issue. It was a failure to follow the PCI DSS standard. British Airways paid the price for ignoring it.

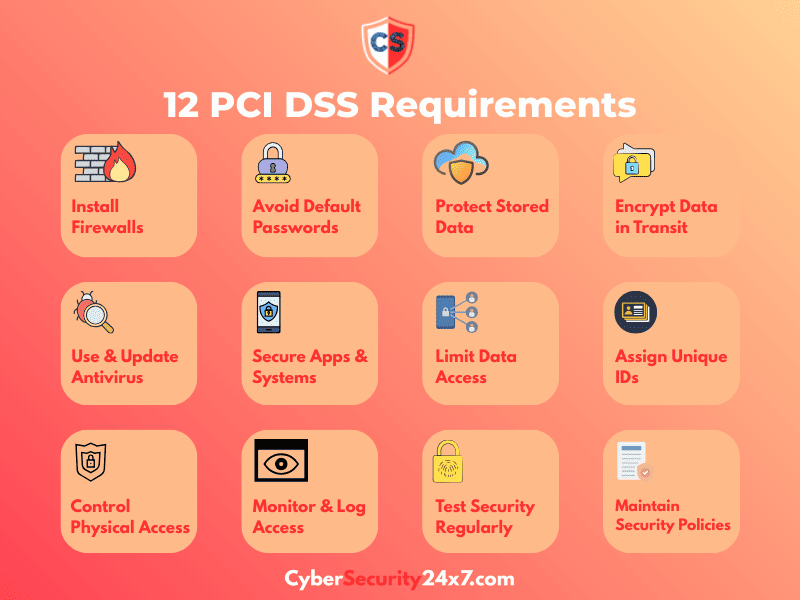

12 Requirements of PCI DSS

Below, we have presented a list of 12 PCI DSS requirements :

Requirement#1: Install and Maintain Network Security Controls

Firewalls establish boundaries between trusted and untrusted networks and help prevent unauthorized access to cardholder data.

Use firewalls to isolate cardholder systems.

Apply network segmentation to reduce CDE exposure.

Review firewall and router configurations every 6 months.

Restrict traffic to required ports, protocols, and services.

Monitor firewall traffic and block unauthorized connections.

Requirement #2: Apply Secure Configurations to Remove Vendor Failures

Factory-set default credentials are easy targets for attackers. All defaults must be changed before systems go live.

Change all default passwords and disable default accounts.

Remove unnecessary services and software.

Enforce strong, unique credentials for users.

Block use of shared or default passwords across systems.

Follow NIST-aligned password policies.

Requirement#3: Protect Stored Cardholder Data

Stored cardholder data must be encrypted, limited in scope, and securely managed to reduce exposure if compromised.

Store cardholder data only if absolutely necessary.

Encrypt stored PAN using strong algorithms (e.g., AES-256).

Mask PAN to show only the first six and last four digits.

Never store CVV, PIN, or sensitive authentication data. post-authorization.

Implement key management procedures and log all key access.

Purge unnecessary data every quarter.

Requirement#4: Encrypt Transmission of Cardholder Data Across Open Networks

Data-in-transit must be encrypted to protect it from interception across public or untrusted networks.

Secure all data exchanges with third-party providers.

Manage certificates and encryption keys properly.

Requirement# 5: Protect All Systems Against Malware

Malware protection is required for any system that could be exposed to threats, not just those storing cardholder data.

Install anti-malware tools on all vulnerable systems.

Keep virus definitions and software updated.

Run regular scans and generate scan logs.

Monitor threat landscape for new malware variants.

Include antivirus installation in baseline system hardening.

Requirement#6: Develop and Maintain Secure Systems and Applications

Vulnerabilities must be identified, prioritized, and remediated across custom code, third-party software, and infrastructure.

Apply security patches as soon as feasible based on risk.

Implement secure coding practices during development.

Limit access to source code and development tools.

Scan applications and infrastructure for known vulnerabilities.

Train developers in secure coding and DevSecOps practices.

Requirement #7: Restrict Access to Cardholder Data by Business Need-to-Know

Only users who require access to cardholder data to do their job should have it. Access must be justified and documented.

Define user roles with minimum required privileges.

Approve access requests before provisioning.

Enforce just-in-time access where applicable.

Remove access immediately upon role changes or terminations.

Conduct regular access reviews and audits.

Requirement#8: Identify and Authenticate Access to System Components

Access must be traceable to specific users. Multi-factor authentication is required for all access to cardholder data environments.

Assign unique user IDs to every account.

Prohibit shared credentials across users.

Enforce MFA for all CDE and admin access.

Require strong passwords and credential hygiene.

Log and monitor all login activity.

Requirement# 9: Restrict Physical Access to Cardholder Data

Data must be protected from physical threats like theft or unauthorized access to storage areas or payment hardware.

Limit facility access to authorized personnel only.

Secure storage of hard copies and portable media.

Install physical security controls (e.g., locks, cameras, ID cards).

Retain physical access logs for 90 days.

Shred or destroy unused data-bearing media securely.

Requirement# 10: Track and Monitor All Access to Network Resources and Cardholder Data

Organizations must retain and review logs to identify and respond to suspicious activity and maintain accountability.

Collect logs for all access to systems processing cardholder data.

Use a SIEM or centralized logging solution.

Retain logs for 12 months.

Preserve user ID, timestamp, system accessed, and activity type logs.

Review logs daily for anomalies.

Requirement#11: Regularly Test Security Systems and Processes

Continuous testing ensures that new vulnerabilities are identified and remediated before attackers exploit them.

Perform quarterly vulnerability scans using an ASV.

Conduct internal and external penetration testing annually. Test systems after significant changes.

Monitor for unauthorized wireless devices.

Use file integrity monitoring to detect unexpected changes.

Requirement# 12: Maintain a Policy That Supports Information Security

Security policies must align with business objectives and guide day-to-day decision-making around access, behavior, and response.

Maintain a formal information security policy and update it annually.

Train employees on secure handling of payment data.

Conduct annual risk assessments and document findings.

Define rules for acceptable use of technology and data.

Establish incident response procedures for data breaches.

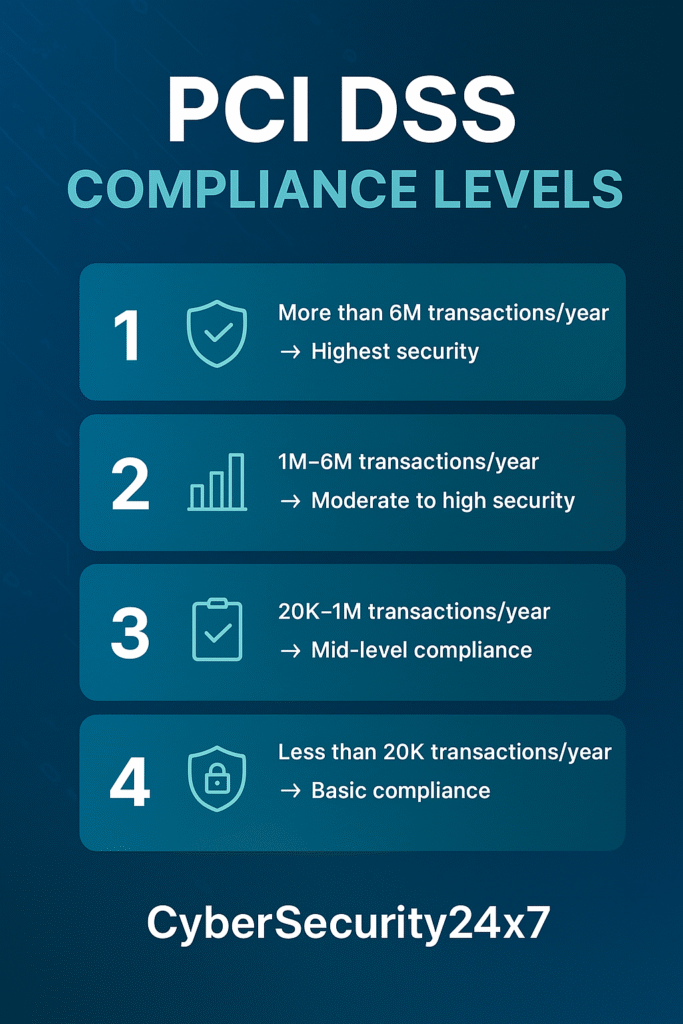

PCI DSS Compliance Levels

Data handling scale varies from company to company. Not every business handles payments at the same scale. PCI DSS takes this factor into consideration. The compliance requirements change based on how many card transactions you process in a year. Here’s how the levels break down:

Level 1 This is applicable For businesses handling over 6 million transactions annually. It faces the strictest requirements, including a full on-site audit by a QSA and quarterly network scans by an ASV.

Level 2 This applies to companies processing between 1- 6 million transactions annually. They may need quarterly scans, depending on their risk profile.

Level 3 This is applicable to businesses processing 20,000 to 1 million ecommerce transactions annually. Like Level 2, they usually need an annual SAQ and quarterly ASV scans.

Level 4 This is applicable to companies processing up to 20,000 transactions per year. These businesses still need to complete an SAQ, and some acquiring banks may ask for quarterly scans too.

To know more about PCI Compliance level, click here.

PCI DSS: Resources And Guide

Want to dig deeper? You can visit the PCI Security Standards Council website. It’s a comprehensive resource library on the topic.

You can also get a PCI Standards overview, FAQs, a glossary, and a quick reference guide that breaks down the essentials.

Bottomline

However, this is not just about card processing volume. The nature of Some businesses are inherently riskier than others. They may have to follow stringent requirements despite lower card processing volume. Banks and card brands may adjust requirements based on breach history or risk profile, and not just volume.

Ignoring PCI DSS can be risky. Contact us now to know how our experts can help.